Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Markets Now FOX Business December 12, 2012 1:00pm-3:00pm EST

1:00 pm

take a look at how stocks are at session highs. everyone rallying on the news that the fed is hard at work. lori: everyone loves stimulus. we will wait to hear from the man himself. bernanke about to take to the podium for a news conference in and hour. melissa: vowing to work through christmas break until a deal gets done. democratic congressman john carney joins us with his take. our own nicole petallides is standing by on the new york stock exchange.

1:01 pm

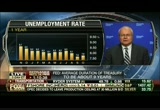

nicole: you are seeing back-and-forth action on the dow jones industrials. they do seem to like it because basically it is the fed putting everything on a silver platter here and is giving it to the world and printing more and find more. it is doing that for an extended period. the people on wall street are saying what are they trying it to unemployment rates you saw the market selloff and now regain its footing. you do the qe forever. gold will be something that we should take a look at. the dollar is something that we have watched slipping away. it is continuing to do that. we have seen things and drugs doing well.

1:02 pm

the dow jones industrials are up they have of a percent for the sixth day in a row. people were thinking that the fed would have a very accommodative sense. one of the things that we should look at is the market is very reactionary. the truth of the matter is they are not pulling anything and they are not raising rates anytime soon because the economy is not sustainable on its own. while you are seeing some minor improvements here and there, the truth of the matter is the economy cannot do it on its own. back to you. melissa: nicole, thank you so much. lori. they will let operation twist expire. expressing disappointment with the pace of recovery employment.

1:03 pm

let's bring in the chief investment officer of merck investments to weigh in. axl, it is great to see you. this is where i want to start. we have had years of quantitative easing. what has it done for the economy so far? >> it has certainly helped the price of gold. let's think about why the fed is doing that. the reason the federal reserve is doing it is because at some point, we will get economic growth. the bond market filling up means higher cost. do not worry about economic growth, per se. we worry about the unemployment rate. they do put in this language here that should inflation go up

1:04 pm

to 2.5%. that is a bad joke. it is a bad joke because the expectations will jump around. they do that to keep the market. they want to move away from focusing on inflation. it is quite surprising that they are able to agree to that so quickly. ashley: john, you say they want to target the unemployment rate. that implies that they think monetary easing is impacting? >> it has improved. that has led to an increase. more workers are producing household appliances that in the past. this has prompted more

1:05 pm

businesses to go out on the risk curve because they find it somewhat easier to obtain reasonably. melissa: we are having the worst recovery that we have ever had. i do not see the connection. it is not like housing has had a booming recovery as a result of their policy. without the fed assistance, we may have been even worse off or going to a more volatile recovery. we know very well that the unemployment rate is significantly lower because of a very high rate of labor force dropouts. we would not have the unemployment rate at 7.7% if it was not for such a low labor force participation rate.

1:06 pm

the unemployment rate ought to be up above 8.9%. we have to be careful choosing these targets. macroeconomics is not a science. lori: let me send it back to you, axl. it is really just troublesome. i was looking at the inflation rate on the ten year period the tenure tip is at 2.6 versus 1.6. are investors willing to take a negative return just for safety.

1:07 pm

>> those inflation expectations are skewed a bit. we just heard it. had the fed not done this, we would have had a more volatile recovery. what the federal reserve wants to do, they want to bail out the ones that are underwater on their mortgage. they want to push up their price level. everything else is just lip service. some jobs are being generated in this process. you have destroyed a whole bunch of purchasing power. obviously, some of that is a political decision. the question is whether the federal reserve should really be in the game of politics. >> we can stay away from these

1:08 pm

policies. the federal reserve could've said you guys in congress need to make up your mind on where you want to take this country to. you do whatever you do. the only time is if policymakers are forced to do so by pressure of the bond market. we don't have that. in some ways we are lucky. it does not mean that we are fiscally sustainable. melissa: john, axl is dead on. >> first of all, if we are going to have a problem with inflation,. [talking over each other] >> the bank of japan has been going through this process since 2001 did japan still suffers

1:09 pm

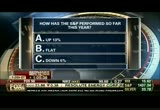

from price inflation. my guess is inflation in japan would be worse if the assets had not succeeded 30% of japan's gdp. japan has a surplus. [talking over each other] >> it has nothing to do with monetary policy. lori: you are both talking simultaneously. i will say thank you both very much. lots of stuff to chew on. it is a difficult challenge. all of this worrying going on in washington, d.c. there is no easy answer. as we approach the end of the year, though, how do you think the s&p 500 has performed so

1:10 pm

far. though surprising results of a new survey on investor sentiment and it turns out perception does not mean reality. melissa: take a look at oil. no decision on who is going to replace the secretary-general as we told you yesterday. i want to show you metals as we go out to break. also rallying. gold is up seven tenths of a percent. we will be right back. ♪ ...so as you can see, geico's customer satisfaction is at 97%.

1:11 pm

mmmm tasty. and cut! very good. people are always asking me how we make these geico adverts. so we're taking you behind the scenes. this coffee cup, for example, is computer animated. it's not real. geico's customer satisfaction is quite real though. this computer-animated coffee tastes dreadful. geico. 15 minutes could save you 15 % or more on car insurance. someone get me a latte will ya, please? we believe the more you know, the better you trade. so we have ongoing webinars and interactive learning, plus, in-branch seminars over 500 locations, where our dedicated support teams help you know more so your money can do more. [ rodger ] at scottrade, seven dollar trades are just the start. our teams have the information you want when you need it. it's anothereason more investors are saying... [ all ] i'm with scottrade.

1:14 pm

♪ melissa: we are making money with charles payne. before the break, we ask you, how do you think the s&p 500 has performed so far this year. the answer is it is up. joining us now is charles payne. they actually thought that they did not realize it was up 13%. i do with individual investors every day. almost all feel like the market is doing better than they are. they always think the market is

1:15 pm

crashing. for me, it is so painful to see this. people have missed out on amazing opportunities. february march 2009, america sold $50 billion worth. lori: what do you think most influences people's perception of the market. first of all, the crash hurts a lot of people about. i think, also, the social security debate, the idea that we would put money into social security into the stock market, that brought a conversation for a lot of people who never thought about the market. they still have this bitter taste in their mouth.

1:16 pm

chasing performance is something that is out of this world. right now, of course, a lot of people are saying we have a bond bubble. pension funds use up 60% in equities. it is absolutely amazing what is happening here. the equity participation overall has dropped dramatically. ten years ago, it was 51%. it has dropped absolutely dramatically. a lot of people feel like, you know, we just do not have our act together. [talking over each other] melissa: it is just one man. imagine this, you are at your retirement party. you just turned 65.

1:17 pm

we are going to take that around the world cruise now. no. we don't have any money because i hated obama. are you kidding me? melissa: charles payne, thank you so much. charles: guess who got hit by that. sir isaac newton. lori: let's check the market with nicole petallides. we were going to touch on dupont. i want to focus more on walmart. this is the biggest loser on the dow jones industrial. the ceo is stating the obvious.

1:18 pm

buyers are feeling the pinch of a soft economy. we talked about the 2.2 million employees they have worldwide. they pay 8.81 an hour. little things such as little things. the bangladesh fire in a factory. right now, they have labor rights and labor unions after them. they have so many things to juggle. the big picture is stuff for walmart. melissa: thank you. what the feds are calling the largest ever insider-trading case. charlie gasparino has exclusive details in my case. lori: you see a weaker dollar today.

1:23 pm

>> @22 minutes past the hour i have your fox news minute. the gunman wearing a hockey mask killed two before taking his own life at a shopping mall in portland yesterday. he fired at random. there is no connection between the 22-year-old and his victims. a 22-year-old woman remains in critical condition. a massive gas line explosion. it also destroyed multiple homes. it left roughly an 8-foot section thanked by the heat. the cause of the explosion is under investigation. green bay packers quarterback aaron rodgers. it has been declared aaron rodgers day today in that state. plans also calling for charity donations to number 12's favorite cause. those are your headlines.

1:24 pm

back to lori and melissa. how important is it that steve cohen is pain the legal fees of a four-month trader. investigators are trying to get the slip against his old boss. here is charlie with the very latest. there is two schools hit. number one as companies often paid legal expenses. we should point out that the former hedge fund trader that is at the center of the latest allegation of insider-trading left about two years ago. he is two years out of it.

1:25 pm

steve cohen is likely to have some sort of cooperation agreement. they share documents. they share strategy. if and when he ever cooperates, and we do know that we want him to cooperate, he still says no. if he ever does cut that deal, he is facing 20 years in jail. if he wants to avoid 20 years, he will know exactly what to say to prepare his defense. the government would only give it to him if he could basically tell him about what steve cohen new about the insider trades that he was accused of.

1:26 pm

in the indictment, it says that bythat -- he traded those stocks based on insider information. he was not supposed to do that. then he told steve cohen something that caused steve cohen to trade those stocks. we should point out also, the largest insider-trading case and probably, in recent history. something like $270 million of ill-gotten gains. we do not know if he has told him i am facing these traits on illegal information. we just know that he talk to him. you talk to a lot of people on the street. we still do not know that information and how it was conveyed. that is what the government wants. tell us what you said. how you said it. did steve cohen no it was inside legal information.

1:27 pm

melissa: it seems like a conflict of interest. charlie: it is completely legal. his contract may not have said we give you, you know, we give you lawyers until the day you die. it would be interesting to know if they cut this deal to pay for the lawyers even though it was not in the contract. we do not know that. we just know that they are paying for it. the suspension is that we have not gotten this confirmed, peter henning is they have a cooperation agreement.

1:28 pm

that would be a huge leg up with martoma ever does cooperate. he knows essentially what he will say. melissa: 19 days to go until the fiscal cliff congressional republican leader vowing to stay in washington until a deal gets done. lori: we will get john carney's take on all of this right ahead. here are some losers and winners on the s&p 500. ♪ can i help you? i heard you guys can ship ground for less than the ups store. that's right. i've learned the only way to get a holiday deal is to camp out. you knowwe've been op all ght. is this a trick to get my spot?

1:29 pm

[ male announcer ] break from the holiday stress. save on ground shipping at fedex office. governor of getting it done. you know how to dance... with a deadline. and you...rent from national. because only national lets you choose any car in the aisle... and go. you can even take a full-size or above, and still pay the mid-size price. this is awesome. [ male announcer ] yes, it is, business pro. yes, it is. go national. go like a pro. [ male announcer ] how could a luminous protein in jellyfish, impact life expectancy in the u.s., real estate in hong kong, and the optics industry in germany? at t. rowe price, we understand the connections of a complex, global economy. it's just one reason over 75% of our mutual funds beat their 10-year lipper average. t. rowe price. invest with confidence. request a prospectus or summary prospectus

1:30 pm

with investment information, risks, fees and expenses to read and consider carefully before investing.

1:32 pm

>> nicole petallides standing by. and our since the fed decision to launch a new bond buying programs so where are markets now? nicole: more bond buying, more money, but the market says thanks, ben bernanke and friends. we know the votes went through, and 11-1 decision. the market's acting this and running with it and moving to session highs so that these are session highs of 76 points on the dow jones industrials, a gain of 1/2%. the ticketing nasdaq is the worst of the month but it isn't 1/3% and the s&p 5 uuder the 0.3% and the s&p 5001430. anyone watching yesterday, he talked about the bias to the upside, talked about 1430 and talked about heading to 1440 and we are not are off of that level. american express leading the

1:33 pm

way. >> no deal to avoid the fiscal cliff, john boehner keeping the dialogue going and even trading new proposals but not stopping them from calling each other out. rich edson is in washington. >> that usually stops or pauses at the very least when there is progress. democrats and republicans have been stuck for weeks. the white house reduced its offer on tax increases for $1.6 trillion to $1.4 trillion including a willingness to begin corporate tax reform. republicans santa white house has to embrace significant spending cuts. >> during our budget we had no new revenue. look at the president's but he has $1.6 trillion worth of new revenue in his budget. we have been reasonable, responsible in our approach to this and we will continue to do that. time for the president to do his

1:34 pm

part. >> democrats say republicans have secured a one trillion dollars in spending cuts, part of last year's the deal and it is time to tax the wealthy. >> it is like a charlie brown cartoon. how many times, how many times is charlie brown going to try to kick that football? we know every time he approaches that football it will be taken away from him. that has happened and we are not going to fall for that again. >> white house officials tell fox republicans continue to refuse to raise tax rates on wealthier families, the official claims that concession would open the pathway to deal. however republicans and democrats are still hundreds of billions of dollars apart on how large a tax increase congress should pass and how much spending it should cut. activists -- back to you. >> there making comparisons to charlie brown. that is the level we are. melissa: for more on the fiscal cliff, let's bring in congressman john carney from capitol hill.

1:35 pm

i am sure you heard the conversation before you. how close are we getting to solving this problem? >> it was a good characterization of where we are and the analogy with the peanuts characters in some ways appropriate. this is what you can expect with both sides talking about what they want, what they are willing to do and opening positions and moving a little more deliberately or slowly, frankly, to an agreement. melissa: is that movement going on? from the sidelines it looks like everyone sticking to their guns, we are not getting closer to resolution. meanwhile the clock is ticking. >> tremendous movement if you consider the difference from two or three months ago to where we are today where the republican side has considerable revenue on the table. the issue is the increase in

1:36 pm

rates versus tax reform which is an important item and on the other side, concern about specificity with respect to spending cuts and both need to happen. a number of members are interested in seeing an agreement presented to us, if it is going to be an agreement that is going to be worked there will be things we don't like. lori: as secretary of finance in delaware you are known for cutting taxes, the first aaa bond rating in the where history. that is an incredible accomplishment. you have written extensively on how to rein in deficit spending but where do you stand? marie e. reference to this, call for 1 pour $4 trillion in revenue. attacks rates go up for the wealthiest americans? >> i think it should. that is the baseline on all the responsible plans to address the fiscal situation. if we do this, i am very optimistic about what the economy will do and what the markets will do in the future. a lot of good things on the horizon. we have to do our business in

1:37 pm

washington. got to come up with an agreement that is balanced and markets have to interpret it as being real. lori: democrats are not agreeing to deeper spending cuts. would you be amenable to more spending cuts? >> we have to have spending cuts. no question. we have to be specific about it. the only way that will happen is to identify a target of spending cuts and frankly tax reform and move into next year, but the committee, the jurisdiction go to address those spending cuts and tax reform targets. lori: if you look at the revenue generated by raising the marginal tax rates if you conceded that it would run the government for a weekend half. do you feel pressured to really reform and slow growth or cut the signs of government to something taxpayers can support? it seems what is coming out of both sides is still a government that can't be supported by

1:38 pm

taxpayers. >> exactly right. we have to have spending cuts. if you look at the framework that the simpson-bowles plan put together, it is $3 of cuts for every dollar of revenue, something on that order needs to be part of the frame work. the most important thing is that we have to bend the spending curbs done with health care across the board for medicaid, medicare, the government programs. talk to any business person as i do in my state and they will tell you health care costs, inflation is killing them. melissa: thanks for joining us. we appreciate your time as always. lori: washington need help from above on the fiscal plan. taking to twitter. we will tell you what he said in 140 characters or less. lori: we are moments from the new complex. what would you like to ask the ben bernanke? melissa: with the tenure and the

1:39 pm

30 year as we head to break. you can see the yield rising on a ten year by 3 basis points. we will be right back. to work h. since ameriprise financial was founded back in 1894, they've been committed to putting clients first. helping generations through tough times. good times. never taking a bailout. there when you need them. helping millions of americans over the centuries. the strength of a global financial leader. the heart of a one-to-one relationship. together for your future. ♪

1:40 pm

>> i am adam shapiro. stocks are getting a boost after the federal reserve announced plans to ramp up stimulus to the u.s. economy. the dow was up 70 points. avon is cutting 1500 jobs from its global work force. the company will also leave south corey and vietnam. the moves are part of a turnaround plan as it is working to eliminate hundreds of millions of dollars in costs over the next few years. honda is going to recall 800,000 minivans and suvs nationwide because the vehicles can roll away even when the key has been removed. recalling. the 2003-2004 model of the honda

1:41 pm

odyssey and pilot suvs and the acura from 2003 through 2006. on the received some complaints including fleet to the cause minor injuries. that is the latest from the fox business network.

1:42 pm

melissa: half an hour from the fed chief's news conference and fox business will bring his remarks live, but first we want to know what would you ask ben bernanke. lou dobbs is here with his take. what would you ask him? >> will will take to get unemployment to 6.5% because that is a new target for the fed. i don't know that in the history of the fed that they have ever put an unemployment target against specific monetary policy. melissa: a lot of times unemployment fall because people ditch the labour market, give up

1:43 pm

looking for job altogether. so is it really an attractive target? melissa: also implied that an impact on unemployment which i'm not sure they do. lou: congress has convinced them of that assigning two targets. it is a two target fed world will live in. not only is it their mandate to forestall inflation but also to forestall unemployment. they have been lousy up the ladder and done brilliantly at the former. now if they conflate these goals and specifically attach a 6.5% unemployment rate as a target for what they're going to do with asset purchase programs and interest rates, that is adventures in the 5 have ever seen it. melissa: wonder if ben bernanke will get into the political fray. he has a rat in previous statements about -- is now or never. lou: it is clear at least to me that he has been in mid vote for

1:44 pm

a weather as a conscious partisan or not but his policies have been designed to inflate the economy and render it cheaper the dollar. lori: you know ben bernanke knows what is best, the best deal, the best situation so if he is going to impose that upon washington today he will share that with us. lou: your words scare us all. when anyone in washington d.c. at the fed or the white house or in congress or the senate thinks he or she knows best we already have of problem because this is supposed to be a government of consensus and direction that is empirically based, operating for two goals, the national interest and the common good. melissa: i thought the role of the fed was to keep money sound, to keep the monetary system roll

1:45 pm

along. lou: so modern, so forward looking. there is something nostalgic in what you say because we have moved well beyond that. this fed right now is in charge of our fiscal future. melissa: these things as our guests have expressed that the economy needs to have the fed do what has been doing to going? lou: ben bernanke has been the essential actor of the last four years because we have had such inadequate leadership from the white house, such inadequate imagination and public policy direction, principal or otherwise partisan or otherwise creative or otherwise, that without him not much would have happened and that would have been absolutely disastrous. i know there are those naysayers

1:46 pm

-- [talking over each other] melissa: we have had that one before. you can see lou any time. 7:00, 10:00 p.m. eastern you can catch congressman dana rocker. look forward to that. lou: egypt and iran and syria and the obama middle east policy whenever it may be. lori: you're looking at costco. >> the largest u.s. wholesale retailer. you get everything in bulk and they obviously have a variety of different items but they came out with some numbers and you will see this stock is not taking off. however not far from the unchanged line, truth is there

1:47 pm

quarterly profit was up 30%. , sales rose 7% and membership revenue, up to the costco member, that rose 14% to $511 million. it seems when you look at the statistics and what the analysts have been expecting they came in with some very decent numbers here and right now the stock is virtually flat but that is a good one showing you the growth. lori: the most highly anticipated tweet, at the first message on twitter saying dear friends, i am pleased to get in touch with you through twitter, thank you for your generous response. i bless all of you from my heart. people follow up that tweet with six more under his twitter handle@pontifex. that is latin for bridgebuilder, eight different languages and already has 1 million followers.

1:48 pm

you should be able to tweak concessions. [talking over each other] lori: everyone for everyone to look at. [talking over each other] lot melissa: and report on what the companies texting coming up next. lori: not a happy holiday for retailers would crashing report for department store stocks. new movers in the trading session as we take a break.

1:52 pm

department, and jailed in guatemala, and did the country. and wanted for questioning in the murder of his neighbors. apple moving in on the living room, the tech giant testing designed for television and shibani joshi has a latest. shibani: the most exciting and clear idea what apple's vision for allen will play, the wall street journal, there's lots of talk. and some sort of accessory or is it going to be a huge flat screen tv that will take a centerpiece in your living room? report out today says it will be the centerpiece item that is going to be what apple is developing next year, it will come out and new prototypes under testing mode right now. it is all of the products, something exciting for the company. melissa: who plus surrounding

1:53 pm

its debut, and -- shibani: apple shares are down today. estimates for sales, came out revising lower is ipad estimates because of the dreaded cannibalization factor. this is what apple, its own worst enemy with new products and people save instead of buying all of its products in the portfolio we are going to take one or two of them. talk about ipad mini supply issues and people not buying the big ipad, there buying the small-lot that and that will affect the bottom line, when everyone is waiting for. to get above $700 or $800 they have been waiting for that for it while. lori: they will shortchange you and then you have to get that number 2 and over to apple for the next few years. shibani: probably going to forever. melissa: citigroup lowering its

1:54 pm

2012 estimates on department stores. j.c. penney, nordstrom, coles and macy's being lowered, shoppers are not spending as much this holiday season. citigroup things warm weather has consumers shined away from cold weather merchandize. additionally online competition, the lack of must have gifts has dampened spending. with a tax increase living, consumers are exercising caution. do you exercising caution? lori: so much conflicting data on holiday sales. better than last year but not downgrading, all over the board. melissa: we will see how it settles a. everyone spends more and they plan to. lori: that is a no-brainer. melissa: without question. lori: are we there right now? melissa: coming up, gordon chan, author of nuclear showdown, north korea takes on the world joining me to discuss north

1:55 pm

korea's long-range missile test. this is the important part as if it weren't enough. reports that iranian officials were in attendance for the launch at 5:00 eastern on fox business. the fear is once they have this technology they start selling it to iran. lori: gordon knows best. melissa: we are 15 minutes or more away from chairman ben bernanke meeting the press. lori: as we compelling stuff. let's check the treasury market as we watch you of to the press conference 15 minutes from now. what our interest rates doing on the back of news? expanding q e, is it q e 4? quantitative easing forever. interest rates are higher, treasuries are selling off as the stock market risess. we will keep these historical interest waits for the time being, that is explicit targeting an unemployment and inflation. people feeling good about u.s. markets and people stopped for a out of fixed-income. there you go. business with market action, trends for today at least.

1:56 pm

melissa: dow trading 67 points and the nasdaq eight ntsb 500 up 9 points. good for 0.6% so markets in positive territory. you know how painful heartburn can be. for fast, long lasting relief, use doctor recommended gaviscon®. only gaviscon® forms a protective barrier that helps block stomach acid from sashing up-

1:57 pm

relieving the pain quickly. try fast, long lasting gaviscon®. at legalzoom, we've created a better place to handle your legal needs. maybe you have questions about incorporating a business you'd like to start. or questions about protecting your family with a will or living trust. and you'd like to find the right attorney to help guide you along, answer any questions and offer advice. with an "a" rating from the better business bureau legalzoom helps you get personalized and affordable legal protection. in most states, a legal plan attorney is available with every personalized document to answer any questions. get started at legalzoom.com today. and now you're protected.

1:58 pm

[ engine revs ] ♪ ♪ [ male announcer ] the mercedes-benz winter event is back, with the perfect vehicle that's just right for you, no matter which list you're on. [ santa ] ho, ho, ho, ho! [ male announcer ] lease a 2013 c250 for $349 a month at your local mercedes-benz dealer. she also likes ride her be. she knows the potential for making or losing money can pop up anytime. that's why she trades with the leader in mobile trading.

1:59 pm

so she's always ready to take action, no matter how wily... or weird... or wonderfully the market's behaving... which isn't rocket science. it's just common sense. from td ameritrade. >> so the market right now up to 65 points. we are seeing gold rally, market happened if it had said they will continue their quantitative easing, officially targeting unemployment. something we've long suspected but now they're coming out and saying it. ashley: the market doing a double take, not sure what to make of it. we will hear from mr. bernanke.

2:00 pm

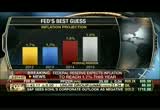

the federal reserve ramping up the action to stimulate the economy. a new round of bond buying in the new year. tracy: the fed says the rates will stay low. the predictions on the economy are out. ashley: fed chairman ben bernanke addressing the press in about 15 minutes. what will he say about the fiscal cliff and so much more? it is all headed. tracy: it'll be interesting with the market when we hear some of the questions. ashley: there will be a lot of questions for him to answer, for sure. tracy: and what if people leave? going down to washington, peter barnes with breaking news. >> that is right. we have the latest economic projections right now from the federal reserve and they are very slight changes from the previous forecast in september. let's run through them starting with the gdp forecast, the fed is now projecting gdp for the

2:01 pm

year 2012 on th on the year wild up with 2013 around 2.7% growth and growth getting a bump reliably in 2014 and 2015. the unemployment rate sees it slightly better compared to september projections. now these unemployment ending up 17.9%. it is a project i prediction ab. 7.6% in 2013, and getting down consistently under 7% by 2015. on inflation, that looks slightly better in this new forecast, 1.7% for 2012, compared to the september forecast of 1.8. and then 1.7, 1.8, 1.9 going out 2015. under 2%, the fed official

2:02 pm

target. we have this handy dandy new chart they have been giving us which is a poll the 19 members, their thoughts on the appropriate timing of policy when they should start to tighten policy. two members believe policy tightening should begin next year, 2013. we begin in 2014, the majority, 13 of them believe it should start in 2015 and one believes the fed should wait until 2016, ashley and tracy, back to you. tracy: peter barnes, thank you very much. ashley: unemployment consistent. on the floor of the new york stock exchange as we do every 15 minutes. nicole petallides, the markets did a double take when we got

2:03 pm

this announcement from the fed but now moving nicely higher. nicole: we have that back-and-forth action as we got the play-by-play. in monetary policy remains much of the same, very accommodated from our fed head. with them doing just that, that basically says we are here for you and we are ready to back just about everything and give the opportunity for the market to continue higher. moving equities to the upside. that is the basis of what we are seeing today. the dow up 70 points. 25 of the 30 dow components a few minutes ago in the green. 25 of 30 names to show you. it is a broad-based rally. we do have the fed, we talked about that. a long winning streak for the dow. we have not seen that in nine months. let's take a look at the fear index.

2:04 pm

it had been higher throughout the day. it certainly was volatile during the lunchtime hour we were hearing from the fed. everybody seems to be taking a breather. back to you. ashley: all right, nicole, thank you very much. the dow up 65 moving higher. tracy: hearing more now from an bernanke and the surprise move to set a targe the target for te unemployment rate. what's do they want to hear? let's bring in our all-star panel. boy, i am sure you have tons of opinions. michael, i will start with you though. most of it was expected, what about this notion of setting it to a target unemployment rate? speak of it is very interesting.

2:05 pm

any polica new policy change fo. the fed really has to wear two hats. one hat is controlling inflation, the other is providing full employment and balanced growth and so on. what they are saying is they're changing the target away from inflation to unemployment and in doing so that means if you can expect a lot more stimulus, more inflation. they will try to give themselves cover creating potentially more inflation and going above the target range. ashley: can we call this qe4, what the fed did today? they are not selling short-term treasuries to upset the purchases, so the balance sheet is getting bigger and bigger and bigger. what do you think of this strategy? is likely the most creative head

2:06 pm

of my lifetime. he has done a pretty good job. we would be in worse shape with the financial fiasco of 2008 if ben bernanke had not been there. tracy: you were at the fed, my first thought when i heard it was tied to unemployment was what if people just leave, people leave the workforce and the number gets that low because tons of people are sitting at home collecting welfare checks. and then what? >> it is a difficult situation in that the unemployment rate isn't the best gauge necessarily tell you how the labor market is doing. the fed has added this qualitative threshold as well now that they're going to be following the labor market conditions in this depends on inflation and inflation expectations and that is why we saw it as early as we did. i don't think anybody was expecting it to be announced today.

2:07 pm

it was pretty clear officials were leaning in this direction, but nobody really expected them to announce it at today's meeting. ashley: more and more money being pumped in. bank reserves getting bigger and bigger, but what can be done to urge them to move the money through the system? obviously they will put money aside for when the rate starts to go up. nevertheless they are reluctant to push the money to consumers and businesses. what good does it do if we give cheap money and they are not passing it on? >> the reasons the banks are not landing. the main one, there are too many rules and regulations. in many cases they don't know if they are breaking the rules or not. excess reserves have gone from less than a tenth of a percent to 16%. we have not had anything like this since 1930. the excess reserves are getting stuck there. access rules and regulations,

2:08 pm

affect the fed has a trap by keeping rates low for so long, there's no place for interest rates to go but up. tracy: you can't blame them. ashley: stay right there, we are moments away from fed chairman ben bernanke taking questions from reporters and a lot of good questions he will have to answer, i'm sure. what will he have to say about the new bond buying program, the economy and more? tracy: but first, let's see how oil is trading in light of all this news up $0.95. $86.73 per barrel. we will be right back.

2:12 pm

ashley: welcome back, everybody. we're awaiting ben bernanke's news conference to set to start in a few minutes. of course we will bring it to you live as soon as it begins. the dow intraday for you. we hear from the fed, little back-and-forth, moving higher consistently. tracy: let's bring our panel back in.

2:13 pm

former analyst at the new york fed. what would you ask the chairman? >> i would ask him when he think the economy will reset itself. i'm of the opinion you will strike a deal with john boehner before the end of the year and he will cave on the 39.6% top tax rate, that will lift the market. he is under a lot of pressure. not only between the two parties but personally the new congress will vote on the next speaker on january 4. if he doesn't cut a deal, cantor has a lean and hungry look. ashley: he certainly does. what would you ask mr. bernanke this afternoon? >> i would probably ask him why the sense of urgency when you are trying to signal that you're trying to keep your foot on the pedal and stimulus policy talking about an exit strategy

2:14 pm

of switching to an economic outcome based approach to guidance rather than the current calendar, what was the current calendar based on the exit of the fed funds rate. it is surprisingly got a consensus view, and i like to hear the other members who probably are not on board were as convinced as the chairman himself. tracy: michael, i'm really hoping you will ask him what his favorite ice cream flavor is. >> i think we need to know how the world of federal reserve is going to get the unemployment rate down. nothing in their tools allow them to do this. it is a function of bad fiscal policy in particular government mandated health care which spot to drive the unemployment rate up again, not down and it's not that the fed has anything in the policy to be able to lower that. we will keep the pedal to the

2:15 pm

metal until the year 2025? until we regain employment 6.5%? who will not be able to add jo jobs, so they get themselves licensed for keeping unemployment rates down for ever. >> you're focusing on the unemployment rate, we raised the possibility of sparking a premature expectation of the fund rate especially if we wind up going over the fiscal cliff and something technical comes out in the unemployment rate drops for some reason. ashley: let's hear from the man himself, mr. bernanke. >> good afternoon. it has been about three and a half years since the economic recovery began.

2:16 pm

the economy continues to expand at a moderate pace. unfortunately however unemployment remains high. about 5 million people, more than 40% of the unemployed have been without a job for six months or more. millions more who say they would like full-time work an have only found part-time employment or stop looking entirely. the conditions in the job market now show waste of human and economic potential. return to broad-based prosperity will require sustained improvement in the job market which in turn requires stronger economic growth. meanwhile apart from some temporary fluctuations largely reflected swings in energy prices, it is likely to run at or below the federal market committee's 2% objective in coming quarters over the longer term. against a macroeconomic backdrop includes high unemployment and subdued inflation, the fomc will maintain the policy.

2:17 pm

today the committee took several steps. first, it decided to continue its purchases of agency mortgage-backed securities initiated at the september meeting at a pace of $40 billion per month. second, the committee decided to purchase longer-term secretary securities after the search to, current program to extend the maturity holdings is completed at the end of the year. in continuing its asset purchases, the committee seeks to maintain downward pressure on longer-term interest rates in the key financial conditions accommodated. therefore promoting economic growth while ensuring inflation over time is close to 2% objective. finally, the committee today also modify the guidance of future rate policy to provide more information to the public about how it anticipates it will react to evil the economic conditions. after discussing our decision to

2:18 pm

turn asset purchases. although the committee's announcement specified amount it pays in composition of asset purchases, did not give specific dates at which the program may be modified or ended. instead, pattern of future asset will depend on evaluation of incoming information in two respects. first call expect to continue asset purchases until we see a substantial improvement in the outlook for the economic price stability. in assessing the extent of progress, the committee will be evaluating a range of labor market indicators including the unemployment rate, payroll employment, hours worked, and labor force participation among others. because increases in demand and production are normally precursors to improvement in labor market conditions, we will be looking closely at the pace of economic activity more broadly. second, the committee will be monitoring financial developments to assess both the efficacy and potential drawbacks

2:19 pm

of the asset purchase program. the federal reserve asset purchases over the last few years has provided important support to the economy, for example by helping to keep interest rates historically low. the committee expects the policy tool to be effective and the cost and risk effect manageable. as the program continues, we will be regularly updating those assessments. if future evidence suggest the program's effectiveness has declined, or potential unintended consequences or risk become apparent as the balance sheet grows, we will modify the program as appropriate. more generally the committee intends to be flexible in bearing the pace of securities purchases in response to information bearing on the outlook were on the received benefits and costs of the program. unlike the explicit arteta criteria associated with the forward guidance about the federal funds rate, which i will discuss in a moment, the criteria the committee will use

2:20 pm

to make decisions about the pace and extent of the asset purchase program or qualitative. in particular, continuation of asset purchases is tied to our seeing substantial improvement in the outlook of the labor market. because we expect to learn more over time about the efficacy of potential costs of asset purchases in the current economic context, we believe qualitative guidance is more appropriate at this time. in today's statement, the committee also be tested the forward guidance for how it expects the target for the federal funds rate dependent future economic developments. specifically the committee anticipates exceptionally low levels for the federal funds rate likely to be warranted. at least as long as the ultimate rate remained up 6.5%, inflation over the time between one and two years ahead is projected to be no more than half a percentage point above the committee 2% longer run golf and longer-term inflation expectations continue to be well anchored.

2:21 pm

this formulation is a change from earlier statements in which forward guidance of the federal fund rate was expressed in terms of a date. for example, in statements the s following a september and october meetings the committee indicated it anticipated exceptionally low levels for the fund rate are likely to be warranted "at least through 2015". the modified for relation makes more explicit the intention to accommodate a stronger economic recovery in the context of price stability. a strategy that we believe will help support household and business confidence and spending. by tying future monetary policy closely to economic conditions, this formation of our policy guidance should make monetary policy more transparent and predicable to the public. the change in the form of the committee's forward guidance is not in itself imply any change in the committee's expectations about the likely future path of the federal funds rate since the october meeting.

2:22 pm

in particular, the committee expects the state threshold from plymouth will not be reached before mid-2015 and projects inflation will remain close to 2% over that period. thus, given the current outlook, the guidance introduced today is consistent with the committee's earlier statements that exceptionally low levels for the federal funds rate are likely to be warranted at least through mid-2015. let me emphasize the 6.5% threshold for the trade should not be interpreted as the committee's long return unemployment. the central tendency estimates of the longer run normal rate of unemployment is 5.2-6.0%. however, because changes in monetary policy affects the economy with a lag, the committee believes it will likely need to begin moving away from highly calmative policy stance before the economy reaches maximum employment.

2:23 pm

waiting until next unemployment is achieved before beginning the process of removing policy accommodation could lead to an undesirable shooting of output and compromise the longer-term employment objective of 2%. that's a statement makes clear, the committee indicates it will be fully consistent with continued progress with employment and staying close the committee's 2% objective over the longer-term. the modified guidance should provide greater clarity of how the committee expects response to incoming data, it by no means puts it on auto pilot. first a statements and notes they view the current low rate policy as likely to be appropriate at least until the specified thresholds are met. reaching one of those thresholds however will not automatically trigger immediate reduction in policy accommodation.

2:24 pm

if a employment were to decline slightly below 6.5% when inflation and inflation expectations were subdued and were projected to remain so, the committee might judge an immediate increase in a target for the federal funds rate to be inappropriate. ultimately in deciding when and how quickly produce policy accommodation the committee will follow a balanced approach in seeking to vacate deviations from a longer run 2% gold and deviations of the estimated maximum level. second, the committee recognizes no single indicator provides a complete assessment of the state of the labor market and therefore will consider changes in the unemployment rate within a broadethe broader context of r market conditions. for example, in elevating a given decline in employment weight, they'll take into the extent the decline was indicated with hours worked in opposed to increased in the number of discouraged workers of labor force participation.

2:25 pm

the committee will also consider whether the improvement of the oncoming freight maintains sustainable. third, they failed to protect inflation between one years and two years ahead of now in terms of inflation. the committee want to look through transitory inflections in affliction such as those induced by short-term variations in the price of internationally traded commodities and to focus instead on the underlining inflation trends. in making its collective judgment about the underlining inflation trends the committee will continu consider a varietyf indicators including measures such as median and core inflation. the use of outside forecasters and the productions to the metric and thi assistive tech models. they will pay close attention to models of inflation expectations to ensure that those expectations remain well anchored. finally, the committee will

2:26 pm

continue to monitor a wide range of information on economic and financial developments to ensure that policies conducted in a manner consistent with our dual mandate. it is worth noting the goals of the fomc's asset purchases in the federal funds rate items are somewhat different. the goal of the asset purchase program is to increase the near-term momentum of the economy by fostering more, and if financial conditions. the purpose of the rate guidance is to provide information about the future circumstances under which the committee would contemplate providing accommodations. i would emphasize a decision by the committee to and asset but committee to end asset purchases when that point is reach would not be titlist to tighter policy. that circumstance the committee would no longer be increasing policy accommodation, policy stance would remain highly supportive of growth. only at some later point would the committee began actually removing accommodations through rate increases. moreover as i discussed today the decisions to modify the

2:27 pm

asset purchase program and undertake rate increases are tied to different criteria. in conclusion, the fomc's actions today are part of our ongoing effort to support economic recovery and job creation while maintaining price stability. as i have often stressed, monetary policy has its limits. only the private and public sectors working together can get the u.s. economy from the back on track. in particular it will be critical that fiscal policymakers come together soon to a suit long-term fiscal sustainability without adopting policies that could derail the ongoing recovery. thank you. i will be happy to answer your questions. >> i have a lot of questions but i will just cough up two here. why are there different targets for q e and the funds rate.

2:28 pm

what has that achieved? secondly, what good is a target if you have to reference calendar dates in that -- you have to point out in the statement is not substantially difficult from the dates we set in september. the do that to make it clear that -- [talking over each other] another paragraph after that says it is not just targeted something else though it is not clear what targets these archie reference the calendar date and the next paragraph is not really targets. >> first, as i said, the asset purchases and the rate increases have different objectives. the asset purchases are about creating near-term momentum to strengthen growth and job creation in the near-term, and the increases in federal funds rate target, when they ultimately occur, are about reducing accommodations, two different objectives.

2:29 pm

secondly, the asset purchases are a less well understood full. we will be learning over time about how efficacious they are, what costs they may carry with them in terms of unintended consequences that they might create and we will be seeing what else happens in the economy that can affect the level of unemployment for example we hope to achieve. for that reason as i discussed in my opening remarks, we decided to make the criteria of for asset purchases qualitative at this time because we have a number of things to look at as we go forward. rate increases by contrast are well understood and we understand the relationship between those with reading greases and the state of the economy so we get somewhat more quantitative specific guidance in that respect.

2:30 pm

with respect to the date and the transition today we wanted to make clear the change in guidance did not happen to be the case that it doesn't change our may of 2015 expectation. going forward we will drop the date and rely on the conditionality and that is imported vantage which is it news comes in that economy is stronger or weaker, then financial markets and the public will be able to adjust their expectations for when policy tightening will occur without the committee having to go through a process of changing in a non transparent way. so that is beneficial. does that cover -- [talking over each other] >> mr. chairman, what prompted

2:31 pm

the committee to make the decision that this particular time to specify targets? and by taking an unemployment rate that is quite low compared to currently, does that shift the balance of priorities in terms of your dual mandate? more in the direction of reducing unemployment rather than inflationary pressures? >> very good question. we took the change today after a good bit of discussion, had a very substantial discussion of the threshold approach that -- had our last meeting and we felt it was ready to go, ready to put out. there are different views and aspects of the threshold approach, there was a lot of agreement that having more explicit connection between rate policy and the state of the

2:32 pm

economy was more transparent and more helpful to the public mandate based guidance, and therefore, a general view that at some point, we should switch to that kind of guidance, we do hope it will be more helpful and give markets more information about how we are going to respond going forward. it is 98 change in our relative balance, towards inflation and unemployment, by no means, first of all with respect to inflation we remain committed to our 2% water run objective. we expect our forecast as you see from a summary of economic projections our forecasts are that inflation will remain despite this threshold of 2.5 and inflation will remain at or below 2% going forward. and so finally the thresholds we

2:33 pm

have put out are entirely consistent with our long standing views on what the rate half has to be, what the path of interest rates has to be in order to achieve improvement in the labour market and keeping inflation close to target. both sides of the mandates are well served and there is no change in policy. it is an attempt to clarify the relationship between policy and economic conditions. >> given that your economic projections are important now, that you have specified these targets, is it difficult to put forward these projections now given the uncertainty over the fiscal cliff? how to sort of plastic are these? >> are you thinking of the s e p

2:34 pm

projections? clearly the fiscal clip is having an affect on the economy, even though we have not even reached the point of the fiscal cliff, potentially kicking in, it is already affecting business investment and hiring decisions by creating uncertainty and pessimism, we see what happens to consumer sentiment which fell because of concerns about the fiscal cliff. this is a major risk factor and major source of uncertainty about the economy going forward. i would suspect, although the participants don't make this explicit, but what they are sitting in their projections is the fiscal cliff gets resolved and some intermediate way, there's still fiscal drag not flags by the entire fiscal cliff so that is the underlying assumption that most people took when they made their projections but you are absolutely right

2:35 pm

that they're a lot of uncertainty right now and the fiscal cliff situation to be resolved in a way different from expectations you would see changes in the forecast. [inaudible] >> thanks very much, mr. chairman. could you talk about whether the decision to maintain the purchase of $85 billion a month represents are ramping up of additional easing of that policy because you are adding a little more to the side of the balance sheet, and also you talked about maintaining the asset purchases and substantial improvement in the labour market and you want to take a different approach but you also have a 6% inflation threshold. could you talk about what sort of evidence you see to make you change the pace or slow theepace

2:36 pm

of purchases? >> the first part of the question was is this an additional stimulus? >> this is a continuation of what we said in september. you recall in september we expressed dissatisfaction with progress in the labour market and at that point began a forty billion dollars per month of them be s purchases and we said we saw substantial improvement in the labour market and undertake additional asset purchases and that is what we have done today is follow for rue what we said we were going to do. relative to last month i don't think we have significantly added to accommodation, the reason at least in my view, many of my colleagues what matters primarily is the mix of assets on the balance sheet, what is

2:37 pm

important is the fact that we are acquiring treasury securities taking those out of the market, forcing investors in to closely related assets and that is where the stimulus comes from, not so much in the size of the balance sheet per se but the amount of stimulus is more or less the same, a follow-through from what we saw in september. in terms of criteria, what we have done is announced an initial amount of $85 billion of purchases, we are prepared to bury that as new information comes, and it is noticeably stronger, we would presumably begin a ramp down, level of purchases. the problem with a specific number is that there are multiple criteria in which we

2:38 pm

make this decision. we look at the outlook for the labour market which is important but we are also looking at other factors that may affect the economy, for example i hope it won't happen but if the fiscal clickers as i have said many times i don't think the federal reserve has tools to offset that event and we have to temper expectations what point accomplished and we will be looking at the efficacy and cost of our program and if we find we expected to be efficacious but it is not working as well as we hoped for various costs we had not anticipated, that will not be taken into account. it was not constructive because we don't know precisely what would be fine a substantial improvement but as long as costs and other concerns do not emerge we will be looking for something

2:39 pm

substantial in terms of a better job market [inaudible] >> peter cook, mr. chairman, if i could follow-up on your last response given the fiscal cliff is it possible if policymakers were not to agree to some sort of deficit deal and we were to go over the fiscal cliff the size of these asset purchases could grow in response to that and more specifically you calling the phrase fiscal cliff and i want your take on whether you feel it is the most appropriate language to describe what will happen at the beginning of the year. some americans may be alarmed, the you feel this is appropriate given circumstances, fiscal contraction that would come if there is no deal? >> the first part of your question, if the economy went off of the fiscal cliff our

2:40 pm

assessment, outside forecasters all think that would have significant adverse effect on the economy and the unemployment rate so on the margin, we would do what we could, we would increase a bit. but i want to be clear we cannot offset the full impact of the fiscal cliff. it is too big given the tools available and limitations on our policy tool kit. in terms of the terminology, people have different preferencess what they call things, the sensible term, the fiscal policies, providing support to the economy if fiscal policy is confectionary the economy will i think go off the cliff. it is reasonable to be concerned about this. i don't buy the idea that a short-term the send off of the

2:41 pm

fiscal cliff would be not possibly. i think it would be costly and we are already seeing costs. why is it consumer confidence dropped so sharply this week? why is that small business confidence dropped sharply? why are the market's volatile? why is business investment among the weakest levels during the recovery? i think all these things to some extent can be traced to the anticipation and concern about the fiscal cliff and we don't know what would happen, but there is certainly a risk that it could be serious and therefore it will be very important that most helpful thing that congress and the administration could do is find a resolution that on the one hand achieved long run fiscal sustainability which is critical, absolutely critical for a healthy economy, and avoids the railing which is in

2:42 pm

process. >> mr. chairman, i wanted to square up some numbers that you announce today when rate hikes start at 6.5%. the committee's assessment of the longer run unemployment rate is 6% or perhaps a bit lower, and in the long run funds rate, it suggests when the fed starts raising interest rates down the road it might have to move fairly quickly to get to some equilibrium funds rate. specifically, is that the case and more generally can you talk about what this framework that you set up today says about the exit strategy that you laid out some time ago on whether that is changing? >> good question. first of all, we don't have a

2:43 pm

precise estimate of the long run sustainable unemployment rate. the estimates that were provided in the summary of economic projections today as has been the case for a while is 5.2% to 6.0%. it could be less than 6.5% so that gives us some time. my anticipation is that the removal of accommodation after the takeoff point where ever that occurs would be relatively gradual. i don't think we're looking at a rapid increase but that depends on where inflation is and other conditions. the path we are basing these numbers on is one that assumes, first of all, as you have anticipated, assumes an increase in the funds rate first occurring some time after

2:44 pm

unemployment goes below 6.5% but it does not necessarily assume a rapid increase after that and what we sit in our statement is we would take a balanced approach. once we get to that point we may or may not raise rates at that point. we will look at the situation. but assuming inflation remains well controlled, which i fully anticipate, the rate of increase in rates would be moderate. this is consistent. the exit strategy that we put out is consistent with our statement today because the exit strategy was primarily about how we would normalize the balance sheet over time and at this time we have not made any changes in that and we believe some increase in the size of our balance sheet is consistent with that general sequence we laid out in the minutes of a year-and-a-half ago.

2:45 pm

that being said, if the balance sheet rose by enough's we may have to reconsider the pace, but i don't see any changes that would radically change the time to normalization or the time to exit. >> i will continue the two question trend. on the fiscal clipped it sounds like you would prefer a sensible balance of fiscal consolidation and support for the recovery but if people in congress can't do that in the next week to week the you think we are setting fiscal consolidation preferable to going over the cliff? and on the monetary policy actions today, can you give more color on how you set the threshold and what they were and what the alternatives were and how you waived various alternatives to similar policies? >> sure. i am hoping congress will do the right thing on the fiscal cliff.

2:46 pm

there is a problem with kicking the can down the road. it might avoid a short-term impact on the recovery, but it could create concerns about our water term fiscal situation. i don't want to see that. for the best interests of the economy to come to a two part solution, part i is to modify fiscal policy in a way that doesn't create enormous head winds for the recovery in the near term and part ii is to at least take important steps towards achieving a framework, at least by which perhaps further negotiation, the congress, administration can achieve a sustainable path for fiscal policy. these are very important. i don't think we could consider these negotiations a success unless both of them happen.

2:47 pm

[inaudible] >> i think they are equally important. on the threshold numbers, this is -- these numbers are based on substantial analysis done by staff both here and at the reserve banks, trying to assess under so-called optimal policy or best policy we could come up with, what would the interest rate half look like and how would it be connected or correlated with changes in unemployment and inflation and when we do that analysis, what we find is the best interest rate half is the best we can determine it based on models and analysis which is imperfect, has rates remaining low until the unemployment rate drops below 6.5% and projects we put in the 1/2% above the 2% goal as a

2:48 pm

protection against any problem with price stability but our projections for actual forecasts suggest inflation will not go there. inflation will stay around to% which is consistent with ponger-term objective. [inaudible] >> if we get important new information about the structure of the economy, it is possible, but i considered relatively unlikely and this is one of the advantages of this approach over the date based approach. informational comes in that the economy is stronger or weaker than we expected that would require a change in the date but it doesn't require a change in the thresholds because the data adjustment can be made by markets just simply by looking at their own forecasts, when unemployment will cross the line and behavior of inflation. >> back of ritter, robin.

2:49 pm

>> scott forin from cnn. on 60 minutes one of the things that happened was you visit your old home town and you talk a little bit about how the economy had affected people you grew up with and affected the people down there. there are a lot of regular people like that on the countryside wondering what really happens to them if we do go over the federal cliff, taxes go up, spending goes down. do they need to look for recession? our employers going to really cut back on the employment? what do people out there really need to worry about and prepare for? when it comes to actually going over the fiscal cliff if folks in washington can't get their act together? >> i come from a part of south carolina which has been

2:50 pm

economically challenged for a long time and remains so. certain parts of south carolina have developed pretty strongly, but the part where i come from, mostly agricultural, a little manufacturing have high unemployment rate, high foreclosure rate and people are having a hard time. i visited very few times since i became chairman. part of the reason we are engaging in these policies is to try to create a stronger economy, more jobs so that folks across the country including places like the one where i grew up, will have more opportunity to have a better life for themselves. that is extremely important and it is very important that we not just look at the numbers. it is easy to look at the unemployment rate and say it is your.1, every tenth means many people are represented there so it's very important to try to

2:51 pm

keep in mind the reality of unemployment, foreclosure, week wage growth, we always try to do that. and i want to -- always a delicate balance. you don't want to scare people, i actually believe congress will come up with a solution, i certainly hope they will. but as many analysts, not just the fed have pointed out, if the fiscal cliff was allowed to occur, certainly if it were sustained for any period, it could have a very negative affect on hiring jobs, wages, economic activity, investment, consequence of that would be felt by everybody, certainly by those in areas like where i grew up that are relatively weak economically no doubt with the

2:52 pm

greater brunch. it is urgent and important congress and the administration come to a sensible agreement on this issue. >> i had a follow-up too. and won't asked if we are on a bond bubble but obviously the new guidance you have given in the fomc statement is going to give a lot more clues to people who own bonds, about when they might start lightening up their bond portfolio and changing the composition of what they own. was concerns about information about bond prices and things happening in a big hurry in terms of some sort of a bubble popping, was that a consideration in adding this transparency? >> i wouldn't say was an important motivation for adding transparency. adding transparency has a lot of

2:53 pm

value, but it is the fact the greater clarity will help markets better predict how bond yields will behave. as we go forward in time as the economy continues to strengthen as we hope, as the exit comes closer for the federal reserve, you would expect longer-term bond yields to begin to rise, the more information we can provide markets about the conditionality under which the fed would consider, the better information they will have about the likelihood of bonds that allow for adjustments so that is a positive aspect of this communication. i would not say it is the major reason. the major reason is to give the markets can the public more transparency about what is determining the policy, but that is one potential advantage. [inaudible]

2:54 pm

>> robin harding from the financial times. mr. chairman, you said a moment ago the threshold there based on an analysis of optimal policy. in the optimal policy part, vice chair yellen wait out in her speech a few weeks ago it showed the first rise in interest rates occurring in early 2016 and rates rising very slowly after that. it has gotten policies that the fed is not following and you referred to a number of inflation forecasts in your introductory remarks. in that case how will we ever know that the inflation threshold has been hit? thank you. >> the kind of policy vice-chairman yeoman showed is indicative of the analysis we have done, a variety of different scenarios, different assumptions about malls and so on but the general character of

2:55 pm

that interest rate half, that it stays low until unemployment is little lower and rise high inflation stays very close to 2. in terms of inflation forecasts, the committee will on a regular basis include in its statement its views of where inflation is likely to be a year from now. currently we already say we expect inflation to run at or

2:56 pm

below the committee's objective longer-term. the intellectual exercise we will be doing is asking if we maintain low rates along the lines suggested by this policy, would we expect inflation to cross the threshold or reach that level. it is very important that the public, the media, the markets find our projections credible obviously. for that reason, we will be referring extensively to publicly available information such as various measures of inflation that i mentioned in my opening remarks, outside forecasts, break-evens from inflation protected bonds etc.. if our outlook deviates in any sense in a significant way from what all these things were saying, at a minimum it would be

2:57 pm

incumbent on me and the rest of us to explain that but my expectation is our projections will be broadly consistent with public views, public information. i think we could manage the credibility issue. just to be clear, the projection that matters for our determination is the one that the committee collectively comes up with. [inaudible] >> you have articulated more clearly than ever your commitment to reduce unemployment but you have also said you are not doing anything more to achieve that goal, you still expected to be three years away, you're disappointed with the pace of progress and inflation is not the limiting factor. what is the limiting factor? why is the fed not announcing additional measures to reduce unemployment? what would it take to get there? >> we took -- the question was if this was renew relative to

2:58 pm

september. september was the date where we did do a substantial increase in accommodation. at that point we announced our dissatisfaction with the state of the labour market and outlook for jobs and said we would take further action if the outlook didn't improve and what we have done today is really just following through what we said. looking at it from the perspective of september, up we have in fact taken significant action to provide support for the recovery and job creation. the reason -- one of the considerations i talk about is given that we are now in the world of unconventional policy that has both an certain costs and uncertain efficacy or benefits, that creates a somewhat more complicated policy decisions than the old style of

2:59 pm

changing the federal funds rate. there are concerns i have talked about in these briefings before that if the balance sheet gets in definitely large, there would be potential risks in terms of financial stability, market functioning, the committee take these risks very seriously. they impose a certain cost on policy that doesn't exist when you're dealing only with the federal funds rate. what we are trying to do is balance the potential benefits in terms of lower unemployment and inflation targets against the reality that as the balance sheet gets bigger, there is greater cost that might be associated with that and those have to be taken into account.

159 Views

IN COLLECTIONS

FOX Business Television Archive

Television Archive  Television Archive News Search Service

Television Archive News Search Service

Uploaded by TV Archive on